Since 1984, Singapore has gone through 4 recessions, of varying intervals between 7 to 14 years. Our last recession in 2008/2009 was sparked off by reckless lending of money from banks to homeowners who took out mortgage loans that were too big for them to handle.

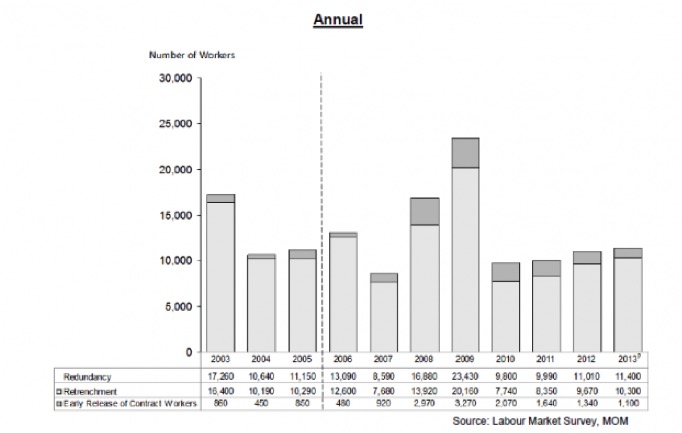

Among other consequences, the last recession caused not only Singaporeans to lose money in the stock markets and through financial products such as the DBS minibonds, but even their businesses and livelihoods. The number of workers made redundant peaked in 2009, and unhappiness over foreigners taking local jobs increased as there was no Fair Consideration Framework then.

It has been 7 years since the 2008 recession. Singaporeans who have not forgotten the impact of the last recession have been bracing themselves for the next recession by reducing debts, increasing savings, adopting a more affordable lifestyle and working out the buffer period they can survive without a steady income. However I believe a large majority of Singaporeans are unprepared and unconcerned. I hope this Singaporean guide on surviving recessions will at least spur you to start your bucket list on what to do before the next wave hits.

1. Will my savings be affected by the recession?

Yes. It depends on what financial products you invested your savings in. A general rule is the higher the promised gains, the higher the risk of losing your investments.

Read the fine print of any products that “guarantee” the principal (or the amount you invested). There may be conditions attached to this “guarantee”, such as:

– holding the product to maturity (you can’t sell it before it matures)

– the guarantor doesn’t go bankrupt (see Lehman Brothers and DBS Minibonds)

Which investments guarantee my savings then?

At the minimum, your savings of up to S$50,000 are insured by the SDIC, if you saved them under:

– A deposit held in a savings account

– A deposit held in a fixed deposit account

– A deposit in a current account

– Any monies placed under the CPF Investment Scheme

– Any monies placed under the CPF Minimum Sum Scheme

– Any monies placed under the Supplementary Retirement Scheme

– Murabaha, as prescribed by the Authority

2. Will I earn less?

Maybe. Your earnings may drop, especially if you usually get big bonuses and commissions tied to your sales or company performance. Even civil servants will not be spared as their bonuses are tied to economic growth.

If you work in industries that are not recession-proof, such as manufacturing, your company may see fewer customers and sales, which affects profits and leads to excess inventory.

On the other hand, you can use the time wisely to second skill yourself in preparation for the economy to pick up again or move to another industry which has better prospects.

3. Will I lose my job?

Maybe. Especially if your company cannot justify your headcount with declining sales.

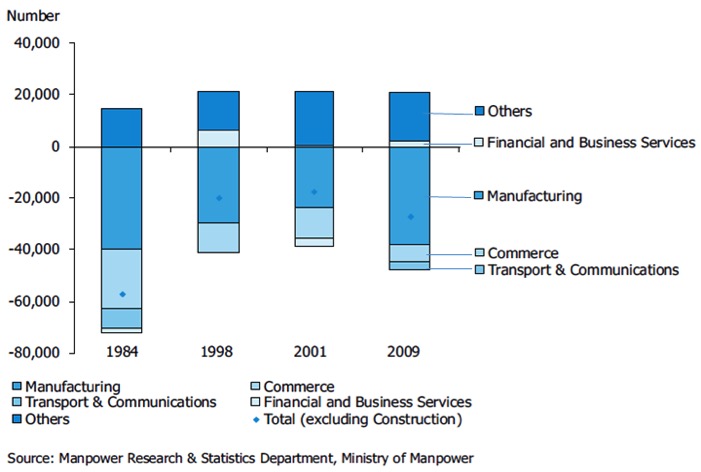

In the last 4 recessions, the number of manufacturing and “Commerce” jobs (e.g. wholesale & retail and hotels & restaurants) shrank, whereas the number of “Others” jobs (e.g. healthcare, education and public service jobs) grew.

4. What should I do if I’m faced with retrenchment?

Prepare for retrenchment in 5 steps here.

Are you a union member? Are you working in a unionized company?

If you answered yes to either, you can check with your union for retrenchment protection and benefits, training and job placement opportunities.

If you answered no to both, you can still contact the NTUC who can point you in the right direction. You should also start updating your resume and participate in job fairs and industry networking sessions. e2i does some of these.

If you’re worried about finding a new job, why not look to new pastures? The following infographic shows 10 jobs that employers have difficulty filling.

Google what qualifications you may require, check if there are WSQ-certified courses you can take, and use your $500 SkillsFuture credit to offset some of the course fees.

Google what qualifications you may require, check if there are WSQ-certified courses you can take, and use your $500 SkillsFuture credit to offset some of the course fees.

5. How did we do during the last recession?

“Cut costs to save jobs, not cut jobs to save costs.” – Lim Swee Say

In the last recession that happened as a consequence of the 2008/2009 financial crisis, Singapore faced retrenchments amid a slowing economy.

Some companies which intended to retrench workers were persuaded by NTUC’s then Secretary-General Lim Swee Say to use the downtime to retrain workers instead (see how he led unions to save both rank-and-file and PME jobs here).

Workers could also upgrade their skills and find new jobs through the SPUR programme (a tripartite effort of NTUC, government and employers). When there were calls to cut employers’ CPF contribution rates to workers, the unions opposed it as it meant the workers would lose out on their CPF contributions. Instead, a temporary Jobs Credit scheme was implemented by the government where employers were paid 12% of the first $2,500 of each month’s wages for each resident worker.

NTUC also raised $23.2 million to help workers. All in, Singapore climbed out of the recession much faster and in better shape than expected.

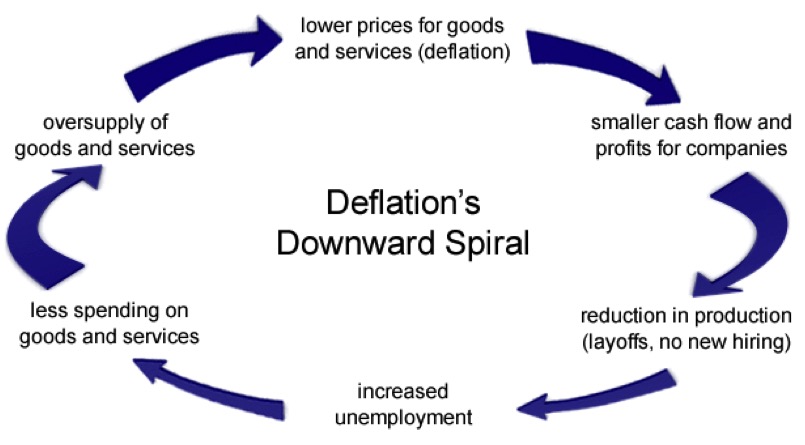

6. We’re experiencing deflation now, will this lead to a recession?

Maybe. To those celebrating the news of deflation (where prices drop) since November 2014, do you know there’s a bigger picture?

Deflation may sound good to the consumer because you pay less, however this also means your company may get less sales.

Since the government has tightened its foreign worker policy, cheap labour is harder to find. This makes the cost of your wages expensive to your company. Are you important enough to your company to avoid the axe?

7. Will my debts and cost of living increase?

7. Will my debts and cost of living increase?

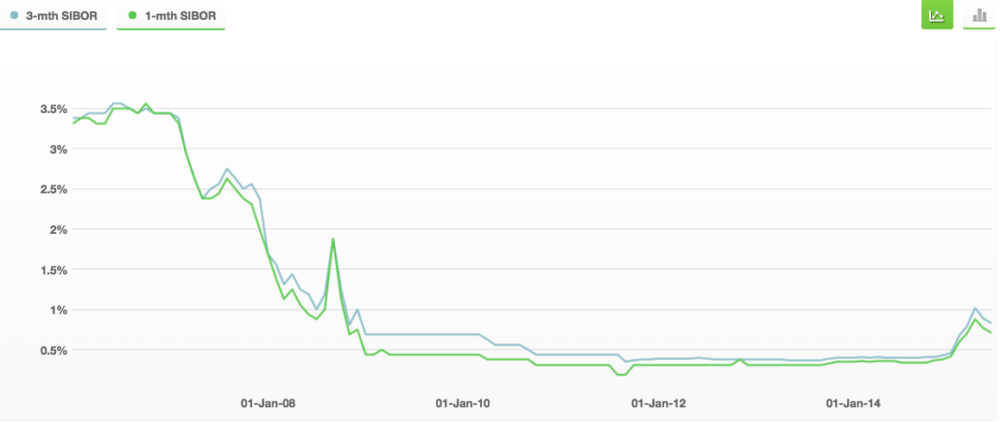

Yes. You should be concerned over whether the interest rates of your mortgage and other debts will rise if your loans are pegged to SIBOR.

If your debt repayments rise, and your income falls, how can you better manage your cost of living to survive periods of unstable income?

You can maximize your benefits from Budget 2015 and try these money-saving tips.

10 Ways to Save Money When Traveling To Or Within Singapore

10 Money Saving Tips To Lower Your Cost Of Living In Singapore

The Singaporean Cheapskate’s Rulebook

30 Money-Saving Life Hacks for Singaporeans

7 simple ways couples can save more money in Singapore

17 Tips To Save Money As A Student