The Central Provident Fund (CPF) has been quite a hot topic in Singapore over the recent years. Created to provide a comprehensive social security system for working Singapore Citizens and Permanent Residents to set aside funds for retirement, CPF also addresses our essential need for healthcare, home ownership, family protection and asset enhancement.

While it is easy to empathise Singaporeans’ frustrations with the rising minimum sum and strict withdrawal limits, I personally experienced how tough it is for policymakers to balance needs, wants and social security as a focus group participant. One would only be able to understand the rationale behind the decisions when tasked to formulate the ‘perfect’ solution for the whole nation.

What’s the rationale behind the Minimum Sum and CPF Life, and how can CPF improve to help us prepare better for retirement? (More info on CPF is available at the end of the article.)

Cannot Take Out At All?

You can withdraw your CPF savings when you turn 55, after meeting your Minimum Sum requirements. The Minimum Sum is set at $155,000 from 1 July 2014 and will be raised gradually until it reaches $161,000 in 2015.

You can still withdraw $5,000 from your SA and OA even if you don’t meet your Minimum Sum.

Rationale Behind Minimum Sum & CPF Life

When the Minimum Sum was first mooted, I was pretty against the idea. I found it ridiculous that the government does not allow me to make decision on how I would want to spend my retirement funds. I jumped at the opportunity to be part of the focus group to give me two cents worth and hopefully be able to convince CPF to make adjustments to the policy. I began to see from the government’s perspective when we were tasked to brainstorm for the entire nation.

1. Protection Against Swindlers

Many of us may think that we are in perfect control of our own finances but is that really the case? When we get old and lonely after our children set up their own homes, it becomes easier for us to fall prey to emotional deceptions and scams. We have already seen significant numbers of old folks who had their entire life savings swindled away, how would they live the rest of their remaining days? As the society becomes more sophisticated, emotional crooks may be able to up their game and target the more educated old folks as well. Wouldn’t you wish you still had an untouched stash when that happens?

For those who think government is locking in my money in CPF, don’t forget how the DBS High Notes investors who lost all their investments in this product after Lehman Brothers declared bankruptcy in 2008. Right after this incident happened, NTUC Secretary-General Lim Swee Say famously told attendees at a financial seminar how “I feel so rich” after looking at his CPF statement (he probably meant “I feel so safe”). You may not feel rich looking at your CPF statement, but you should feel safe knowing that creditors cannot touch your CPF money.

2. Protection Against Poor Financial Management

Even if you are very confident that you will not be a victim of swindlers, are you someone who can manage a sudden influx of funds? Gone are the days of prudent savers, our local banks are no longer encouraging Singaporeans to save. They tell us to go spend, get loan and enjoy instant gratification. What a trap that is, I personally know folks who have at young age chalk up a substantial amount of debts which with their income, it would take years to clear.

3. Think Bigger Than Yourself

It would be selfish to just consider our own wants and ignore the potentially bigger social problems that would surface eventually without the existence of Minimum Sum and CPF Life. Will you be prepared to do your part to clear the shit when it happens?

How Can CPF Retirement Policy Be Made Better?

Of course, the current policy is not perfect and it would be constantly evolving to take care of our changing retirement needs. Out of NTUC’s recommended 15 CPF improvements to help workers, the government announced these changes in the Budget 2015.

1. Help PMEs Prepare For Retirement

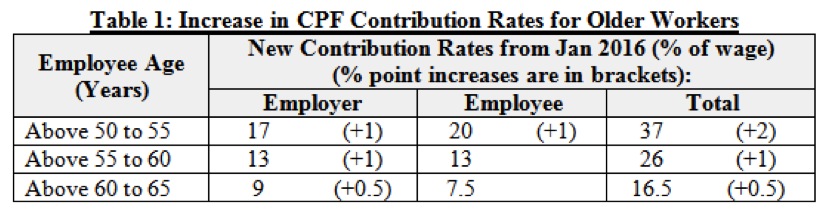

The government will increase CPF contribution rates for workers aged 50 and above, from 1 January 2016.

2. Help Mature PMEs Strengthen their CPF

2. Help Mature PMEs Strengthen their CPF

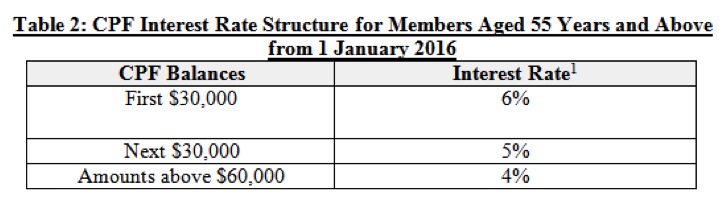

The government will increase the interest rate on the first $30,000 of CPF balances of members aged 55 years and above by 1%, from 1 January 2016.

3. Higher salary ceiling

3. Higher salary ceiling

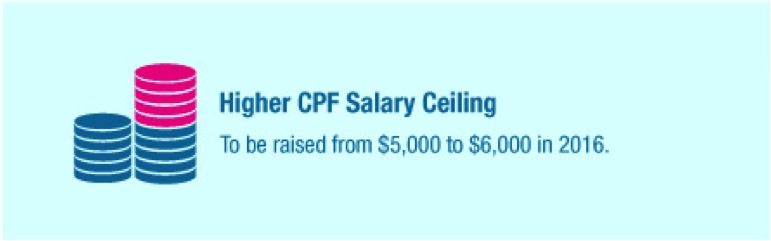

The salary ceiling will be raised to $6,000 so more of us get more CPF employer’s contribution.

For example, you earn $6,000 a month now. If you’re below 55, your employer only contributes 17% x $5,000 = $850 to your CPF. But from next year, your employer has to contribute 17% x $6,000 = $1,020. This is an extra $170 a month, or $2,040 a year!

How To Retire With CPF?

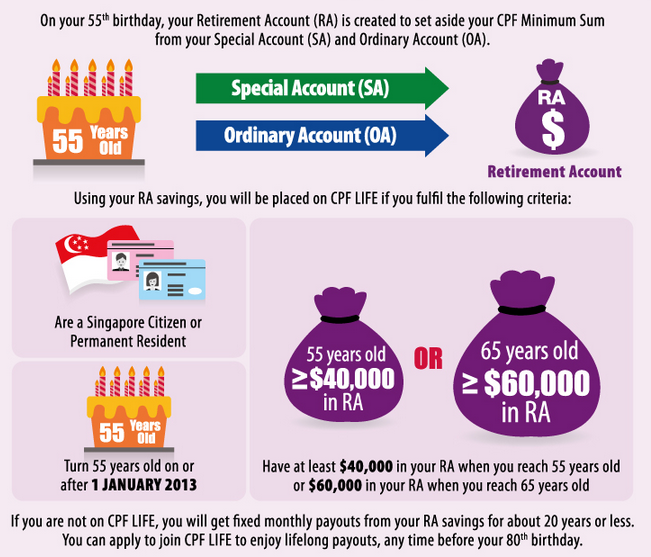

When you reach your 55th birthday, the savings from your Special Account (SA) and Ordinary Account (OA) will combine to form Retirement Account (RA) from which the Minimum Sum (MS) is derived. With effect from 1 January 2013, you will be placed on CPF LIFE if you are a Singapore citizen or permanent resident, born in or after 1958 and have at least:

– $40,000 in your RA when you reach 55 years old; or

– $60,000 in your RA when you reach your Draw Down Age (DDA).

If you are not placed on CPF LIFE, you can join anytime between age 55 and one month before your 80th birthday.

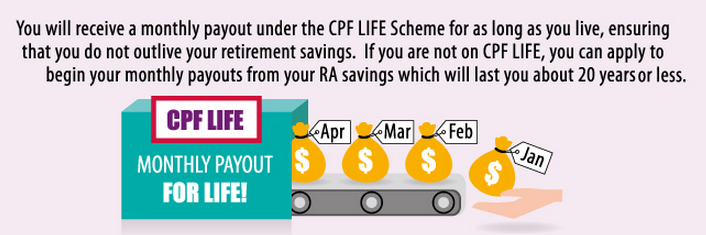

Upon reaching your DDA, you will receive your monthly LIFE payouts for as long as you live. If not, you can apply to commence your monthly payouts from your RA when you reach your DDA and receive the monthly payouts until your RA balance is depleted. Alternatively, to allow your payments to last longer, you may wish to start your monthly MS payouts later.

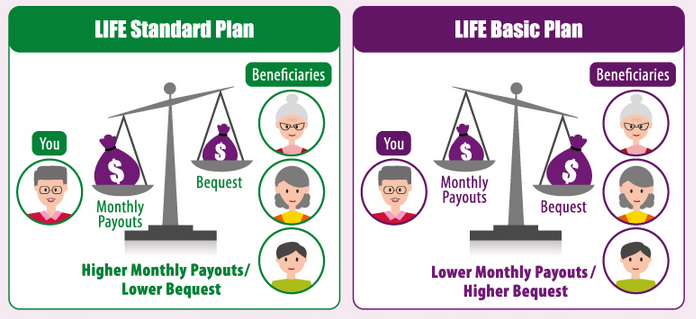

CPF Life Also Got Options

Once you turn 55, you will receive the option to choose from 2 different CPF Life Options – the LIFE Standard Plan and the LIFE Basic Plan. The plans differ on the monthly payout you would receive and the amount you would bequest to your beneficiaries.

Do you feel strongly about CPF Minimum Sum & CPF Life? Please share your thoughts through the comments section below. We would love to hear constructive feedback and suggestions from you.